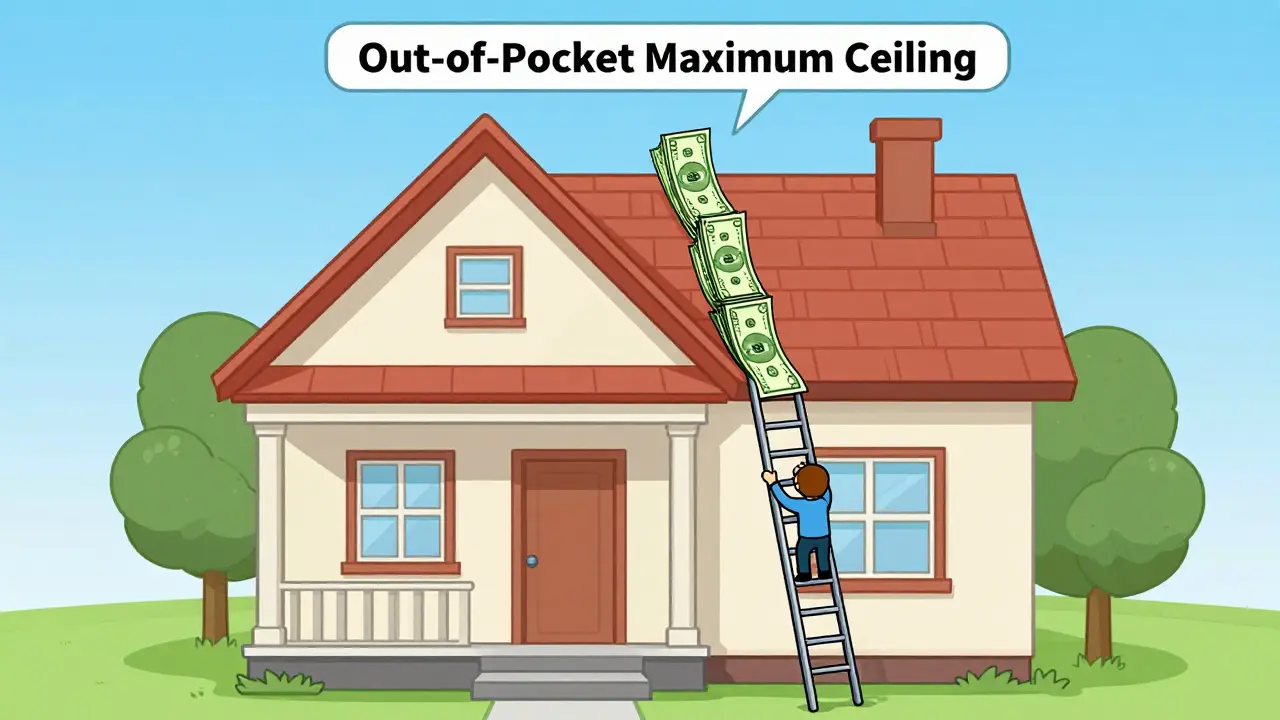

To get a handle on this, we need to look at the ceiling and the floor of your healthcare spending. Think of the out-of-pocket maximum as the absolute ceiling. Once you hit this number, the insurance company picks up 100% of the tab for covered services. The deductible, on the other hand, is more like a threshold you have to cross before the insurance company starts sharing the cost of your care. While they sound similar, they follow different rules when it comes to your pharmacy visits.

The Big Difference: Deductibles vs. Out-of-Pocket Maximums

If you're staring at your plan documents, you'll see two different numbers. One is your deductible, and the other is your out-of-pocket maximum. To understand why your generic drug copays aren't lowering your deductible, you first need to understand what these entities actually are.

Out-of-Pocket Maximum is the most you will have to pay for covered services in a plan year. According to data from Healthcare.gov, for 2026, the maximum limit for Marketplace plans has risen to $10,600 for an individual and $21,200 for a family. This is a safety net designed to prevent a catastrophic medical event from bankrupting you.

Deductible is the amount you pay for covered health care services before your insurance plan starts to pay. If you have a $3,000 deductible, you're responsible for the first $3,000 of medical bills. Only after that point does your insurance start paying a percentage (coinsurance) or a fixed fee (copay).

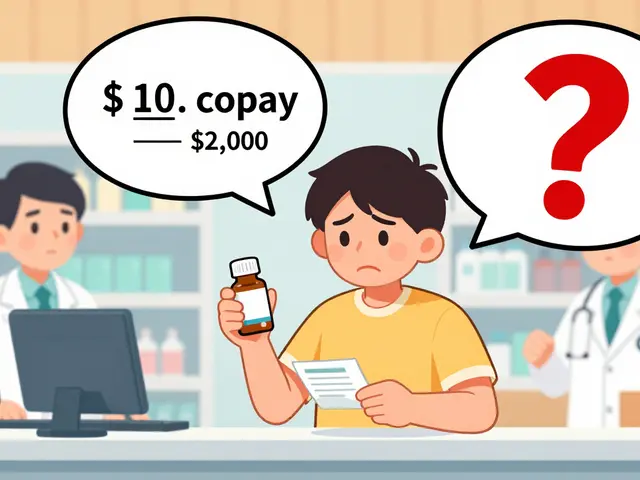

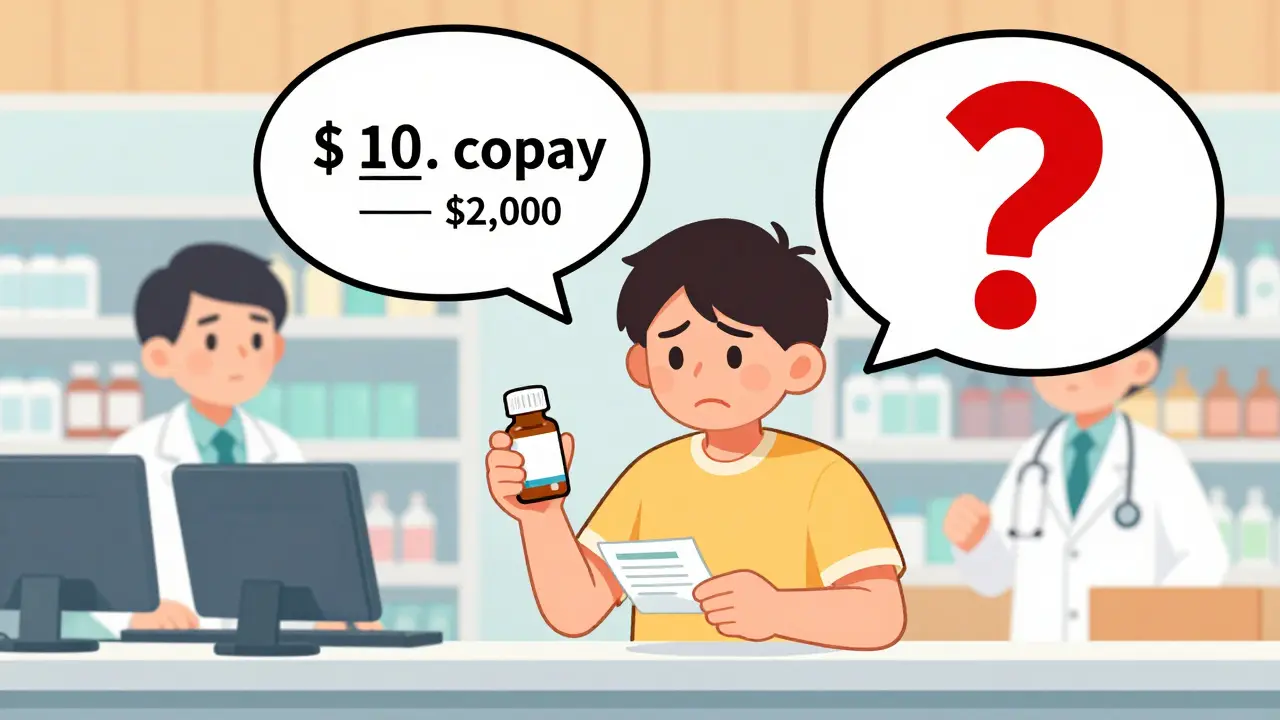

Here is the kicker: Generic copays almost always count toward your out-of-pocket maximum, but they rarely count toward your deductible. This creates a "two-tiered" system where you're making progress toward your annual ceiling, but you aren't getting any closer to the threshold that triggers insurance payouts for other medical services.

How Generic Copays Fit Into the Math

Let's use a real-world scenario to clear the air. Suppose you have a plan with a $1,500 deductible and an $8,000 out-of-pocket maximum. You take a generic medication that has a $10 copay. Every time you pick up that prescription, you pay $10. That $10 is a "fixed cost" that your insurance has already agreed to handle via a copay, rather than a "variable cost" that you must pay in full until the deductible is met.

Because you're paying a flat fee, the insurance company doesn't view that as a deductible expense. However, since the Affordable Care Act (ACA) was implemented, the law requires that all in-network cost-sharing-including those $10 generic copays-must count toward your overall out-of-pocket maximum. Before 2014, those copays were essentially "lost money" that didn't help you reach your limit. Now, they act as small steps toward that $8,000 ceiling.

| Expense Type | Counts Toward Deductible? | Counts Toward Out-of-Pocket Max? |

|---|---|---|

| Generic Drug Copay | Usually No | Yes |

| Emergency Room Visit | Yes | Yes |

| Monthly Premium | No | No |

| Coinsurance (e.g., 20% of bill) | Yes (after deductible) | Yes |

Three Common Plan Structures You Should Know

Not every plan handles prescriptions the same way. Depending on your employer or the plan you bought, you likely fall into one of these three categories. Knowing which one you have is the only way to stop the guessing game at the pharmacy counter.

- The Single Deductible Model: This is the most straightforward. You have one deductible for everything-doctors, hospitals, and drugs. In this setup, you usually don't have a "copay" for generics until the deductible is met. You pay the full negotiated price for the drug until you hit that limit, then you switch to a copay.

- The Separate Prescription Deductible Model: This is where it gets messy. You have a medical deductible (e.g., $2,000) and a separate prescription deductible (e.g., $250). You must pay the first $250 of drug costs before generic copays even kick in. Once that $250 is hit, your copays start, and those copays count toward your global out-of-pocket maximum, but they don't help you hit your $2,000 medical deductible.

- The Copay-Only Structure: This is common in many "richer" employer plans. There is no prescription deductible. You pay a $10 generic copay from Day 1 of the year. These payments never touch your medical deductible, but they do chip away at your total out-of-pocket maximum.

The "Valley of Confusion" and Why It Happens

Policy experts, including those from the Brookings Institution, refer to this as a "valley of confusion." The problem is that we naturally assume all healthcare spending happens in one bucket. When you see your "Total Spent" in an insurance app, it often aggregates everything. But the internal logic of the insurance company separates "deductible-eligible expenses" from "copay-only expenses."

This confusion has real-world consequences. Reports from Modern Healthcare suggest that billions of dollars in necessary medications go unused every year because people misunderstand their cost-sharing. They might avoid a prescription because they think they haven't "reached their deductible yet," not realizing that a generic copay is a flat fee they can afford regardless of the deductible status.

How to Audit Your Own Plan

Don't trust the general summaries. If you want to know exactly how your generics are treated, you need to dig into two specific documents: the Summary of Benefits and Coverage (SBC) and the Explanation of Coverage. These are standardized documents required by the ACA.

When you open your SBC, don't just look at the price of the drug. Look for a column or a note that asks, "Does this payment count toward my deductible?" If the answer is "No" for generic prescriptions but "Yes" for the out-of-pocket maximum, you are in the standard copay-driven model. If you see a separate "Pharmacy Deductible" listed, you're in the separate deductible model.

If you're managing a chronic condition, this distinction is vital. For someone with diabetes, for example, paying a monthly insulin copay that counts toward the out-of-pocket maximum is a huge win. Once that maximum is hit-which happens faster when copays count-the insurance company covers 100% of everything for the rest of the year, including those prescriptions.

Do my monthly insurance premiums count toward my out-of-pocket maximum?

No. Monthly premiums are the cost of having the insurance policy itself. They are not considered "cost-sharing" for medical services, so they never count toward your deductible or your out-of-pocket maximum.

Why does my generic copay not count toward my deductible?

In most plans, a copay is a pre-negotiated flat fee. Because the insurance company has already agreed to a specific price for that service, it is treated as a shared cost from the start, rather than an expense you must pay in full to "unlock" your insurance benefits (which is what a deductible does).

What happens after I hit my out-of-pocket maximum?

Once you reach the out-of-pocket maximum, your insurance company pays 100% of all covered in-network services for the remainder of the plan year. This includes your generic drug copays, specialist visits, and hospital stays.

Does using a generic instead of a brand-name drug change how it counts?

The counting rules (deductible vs. max) are usually the same for both. However, the amount you pay will be different. Brand-name drugs typically have higher copays or may be subject to coinsurance, which can make you reach your out-of-pocket maximum faster but at a higher cost to you.

What if I use an out-of-network pharmacy?

Warning: Out-of-network costs often do NOT count toward your in-network out-of-pocket maximum. This can lead to a situation where you pay thousands of dollars at a pharmacy but are still nowhere near your plan's ceiling.

Next Steps for Your Healthcare Budget

If you are currently in your open enrollment period or reviewing your benefits, take 45 minutes to map out your "worst-case scenario." Multiply your monthly generic copays by 12 and add them to your deductible. If that sum is close to your out-of-pocket maximum, you are in a high-utilization bracket and should prioritize plans with lower ceilings over plans with lower premiums.

For those with chronic illnesses, look for "Integrated Deductible" models if they are available in your state. These newer models are designed to let prescription costs-including copays-count toward a single medical deductible, removing the confusion and potentially lowering your total cost of care.